Claim Synopsis

Viral posts circulating heavily in early 2026 suggest Congress is secretly advancing a unified bill to cut Social Security benefits by twenty percent for current retirees while immediately raising the full retirement age to seventy. You have likely seen these alarming graphics shared across major social media platforms, often accompanied by urgent calls to contact representatives before a supposed midnight vote. We traced these escalating narratives back to heavily edited video clips from recent Senate Finance Committee hearings and politically motivated campaign emails designed to solicit donations. The core assertion driving this panic claims that the Social Security Administration will enforce drastic, permanent benefit reductions this calendar year unless lawmakers pass a new emergency tax measure. These claims have generated significant anxiety among seniors relying on fixed incomes, prompting widespread confusion about the actual state of retirement policy news and pending legislation.

Methodology Note

Our verification process relies strictly on primary legislative texts, nonpartisan budgetary assessments, and official demographic projections. We cross-referenced the viral claims against the most recent annual report from the Social Security Board of Trustees; this document serves as the definitive actuarial gauge of the program’s long-term financial health. Furthermore, our team reviewed active bills indexed directly on Congress.gov to determine if any pending legislation matches the draconian measures described online. We also consulted fiscal audits published by the Government Accountability Office to verify the historical precedent of congressional intervention during past shortfall projections. We ignored all partisan commentary, cable news punditry, and speculative op-eds. By focusing entirely on hard data and verified legislative dockets, we applied our rigorous standard for evaluating economic policy to ensure you receive a clear, unbiased picture of the current legal landscape surrounding your earned benefits.

Evidence Record: The Threat of Immediate Benefit Cuts

The Viral Assertion

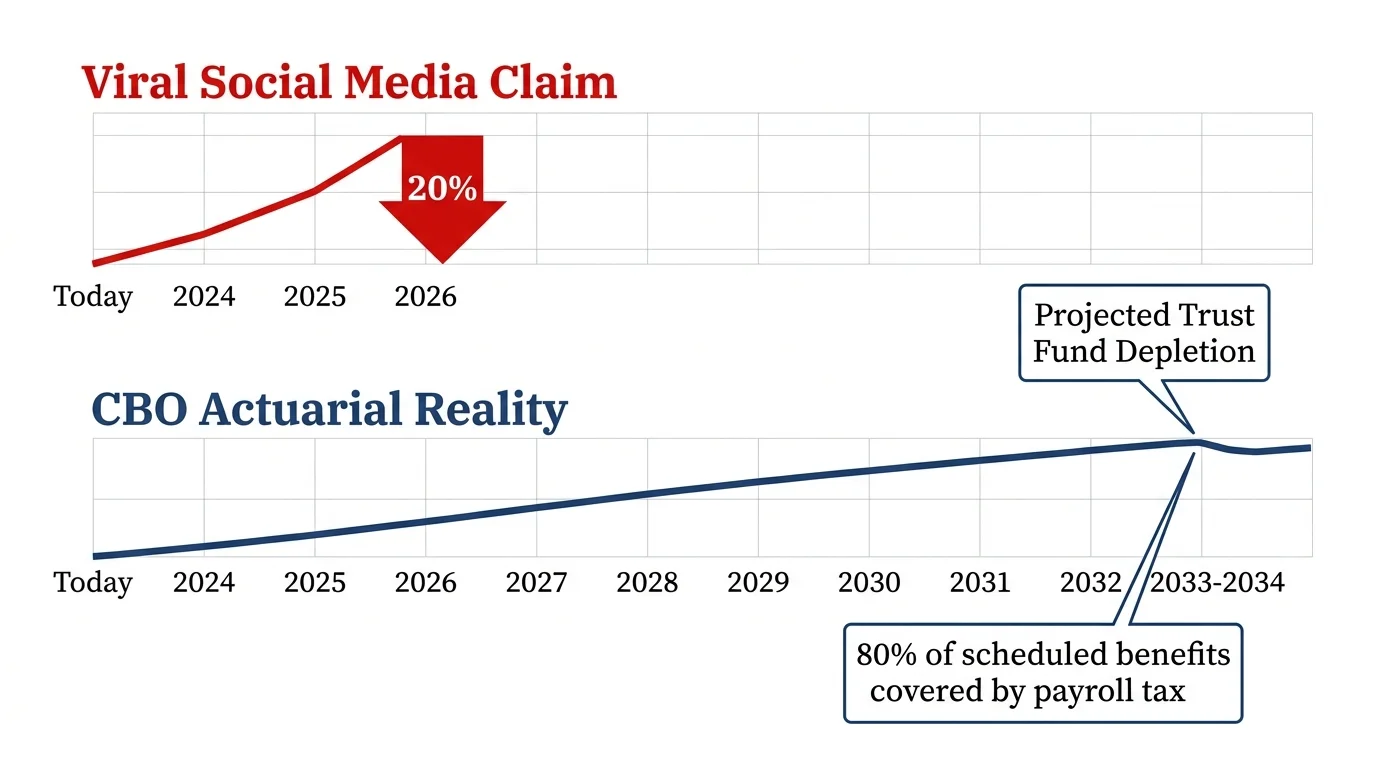

A prevalent component of the viral narrative insists that current beneficiaries will experience an automatic, across-the-board twenty percent reduction in their monthly checks starting in late 2026. Social media influencers claim this cut is a hidden provision embedded in recent federal budget resolutions and that current retirees possess no legal recourse to stop the impending financial loss.

The Actuarial Reality

This claim is definitively false. The assertion fundamentally misunderstands the mechanics of the Old-Age and Survivors Insurance Trust Fund. According to baseline projections from the Congressional Budget Office analysis, the trust fund faces a depletion date closer to 2033 or 2034, not 2026. You must understand that this depletion date represents a future mathematical threshold, not a current statutory mandate. If Congress takes absolutely no legislative action by that future deadline, the Social Security Administration would only be able to pay out benefits from ongoing payroll tax revenues, which actuaries estimate would cover roughly eighty percent of scheduled benefits. The viral claim takes a mathematical projection for the next decade and falsely presents it as an immediate legal reality for this year.

Impact on Current Retirees

Lawmakers are currently debating various solvency packages, but you will find absolutely no active bill proposing immediate cuts to Americans who already receive retirement checks. Historically, Congress exempts current retirees from structural benefit changes to avoid immediate economic shocks and political fallout. The circulating rumors intentionally conflate the projected future shortfall with immediate legislative malice. By examining the actual text of the bipartisan frameworks currently circulating in the Senate, we confirm that all proposed revenue adjustments or benefit modifications explicitly target future beneficiaries—specifically those currently under the age of fifty. The payment structures for those presently relying on the system remain wholly unaffected by the social security reform 2026 proposals currently on the table.

Evidence Record: Raising the Full Retirement Age to Seventy

The Legislative Claim

Another highly shared post suggests a bipartisan congressional consensus has already passed legislation raising the full retirement age to seventy for all American workers, effective immediately. The narrative implies that individuals planning to retire this year must now work an additional three to four years to avoid severe financial penalties.

Distinguishing Blueprints from Law

This assertion is highly misleading. While several prominent think tanks and specific congressional caucuses have published white papers proposing an increase in the retirement age, these documents serve as theoretical policy blueprints rather than binding legislation. You can find detailed, nonpartisan evaluations of these various age-increase scenarios through the Congressional Research Service, which routinely models how incremental demographic changes might affect the program’s long-term solvency. Proposing an idea in a policy brief is entirely different from drafting a bill, moving it through committee markup, and securing enough votes to pass both chambers of Congress. No such legislation has passed either the House or the Senate.

The Timeline Reality

Even when you examine the most aggressive proposals seeking to raise the retirement age, lawmakers structure the increases gradually over several decades. For example, a recent discussion draft suggests extending the full retirement age by just one month per year starting in the year 2030, eventually reaching age sixty-nine by 2054. The viral posts strip away this crucial timeline, falsely implying that workers currently in their late sixties will suddenly face new legal barriers to claiming their full benefits. Changing the retirement age requires complex legislative maneuvering and faces steep, organized opposition from senior advocacy groups. You should view claims of an immediate, surprise age increase as a classic fear-mongering tactic designed to drive web traffic rather than inform the public.

Evidence Record: The Privatization of Retirement Funds

The Investment Narrative

The final major assertion driving the current panic claims that lawmakers are actively drafting provisions to divert your Social Security payroll taxes into mandatory private stock market accounts. Advocates sharing this claim warn that an impending stock market crash will wipe out the retirement savings of millions of Americans because the government has supposedly surrendered control of the trust fund to Wall Street firms.

Current Legislative Actions

We rate this claim as completely false. While the concept of privatization dominated the political discourse during the early 2000s under previous administrations, current legislative efforts focus almost exclusively on adjusting the payroll tax cap, modifying the benefit formula, or finding alternative tax revenue streams. We systematically reviewed the legislative dockets for the current congressional session and found zero bills sponsored by party leadership that attempt to privatize the Old-Age and Survivors Insurance Trust Fund. The system remains a pay-as-you-go program funded by dedicated payroll taxes and conservative treasury bonds.

Independent Verification

Independent researchers at the AARP Public Policy Institute consistently monitor retirement security updates, and their comprehensive legislative trackers show zero movement toward structural privatization. The resurgence of this specific narrative appears to be an artificial recycling of decades-old political attacks. Operatives frequently dust off the privatization threat because it successfully triggers anxiety about financial instability, ensuring high engagement metrics on social platforms. The modern debate regarding SSA changes proposed for the upcoming decade simply does not involve shifting federal funds into volatile equities.

Pattern Watch

When monitoring retirement policy news, you will frequently encounter this specific brand of misinformation during heightened election cycles. Political action committees routinely weaponize the genuine complexities of trust fund solvency to manufacture targeted outrage. The psychological pattern is highly predictable; bad actors take a distant actuarial projection, such as the 2033 funding cliff, and compress the timeline to suggest an immediate, devastating crisis. They also intentionally blur the line between a partisan white paper and a bill actively moving through a legislative committee.

Algorithms on major social platforms heavily favor content that evokes high-arousal emotions, making threats to earned retirement benefits exceptionally viral. By framing theoretical policy debates as imminent laws, these deceptive campaigns exploit the deep reliance millions of Americans have on their earned benefits. You must recognize this intentional compression of time and distortion of the legislative process as a primary indicator of manipulative political messaging.

Accountability Guidance

You possess the tools to independently verify these alarming claims before sharing them or altering your financial plans. Whenever you encounter a distressing headline about Social Security cuts, your immediate first step should be demanding the specific bill number. If a politician, online influencer, or digital advertisement cannot provide an exact legislative citation—such as H.R. 1234 or S. 567—they are almost certainly referencing a vague proposal rather than actual, moving legislation. You should input that exact bill number directly into official government databases to read the actual summary and track its real-time status.

Additionally, you should closely watch how your elected officials speak about the program’s long-term solvency. Hold them accountable for providing concrete, mathematically sound solutions rather than allowing them to rely on the same recycled talking points that fuel online panic. Transparent representation requires clear, definitive answers about both potential revenue increases and specific benefit adjustments. Demand data-driven policy positions rather than emotional rhetoric.

Frequently Asked Questions

What rating standards do we use to evaluate these claims?

We apply a strict, evidence-based continuum that ranges from completely factual to blatantly false. A claim receives a false rating when the primary source documents directly contradict the core assertion. We issue a misleading rating when a statement contains a localized grain of truth—such as the existence of a long-term funding shortfall—but distorts the timeline, scope, or target demographic to deceive the reader. You can trust our ratings because they rely exclusively on verifiable, public data rather than political opinion or secondary analysis.

How do we determine the credibility of our sources?

Our editorial team strictly prioritizes primary government documents over secondary interpretation. We rely heavily on the Office of the Chief Actuary, the Congressional Budget Office, and official committee transcripts because these entities operate under strict statutory mandates to provide nonpartisan data. When we must consult outside experts, we exclusively look for economists and policy researchers who possess a documented history of peer-reviewed publication and bipartisan congressional consultation. You will never see us cite anonymous political insiders, unverified campaign materials, or hyper-partisan blogs as evidence for our fact-checks.

What is the process for submitting corrections?

We maintain a highly transparent and immediate correction policy to ensure our reporting remains flawless. If you identify a factual error in our text, we encourage you to contact our editorial desk with the specific discrepancy and the primary document that refutes our reporting. Our fact-checking team will independently review your submission within twenty-four hours. If we determine a correction is warranted, we will update the article immediately and place a prominent editorial note at the top of the page detailing exactly what was changed, why the change occurred, and how it impacts the overall verdict.

How frequently do we update these legislative fact-checks?

Social security reform represents an evolving legislative landscape, and we monitor the congressional docket continuously. We update our primary fact-checks whenever a relevant bill passes a major committee hurdle, receives a floor vote, or undergoes significant amendment. You can check the timestamp on our articles to confirm currency; however, we also publish distinct, newly dated updates when the fundamental nature of the debate shifts, ensuring you always have access to the most accurate retirement security update available on the web.

Final Verdict

The viral narratives claiming Congress is secretly implementing immediate twenty percent benefit cuts, raising the retirement age to seventy for all workers, and privatizing the trust fund in 2026 are definitively false. While the Social Security Trust Fund faces a genuine, well-documented solvency deadline in the next decade requiring eventual legislative intervention, absolutely no active bill targets current retirees for reductions or introduces immediate privatization schemes. You should completely disregard sensationalized social media graphics that conflate long-term actuarial projections with imminent legislative action. Rely strictly on primary documents, official legislative trackers, and nonpartisan budgetary reviews to stay accurately informed about the reality of retirement policy proposals.