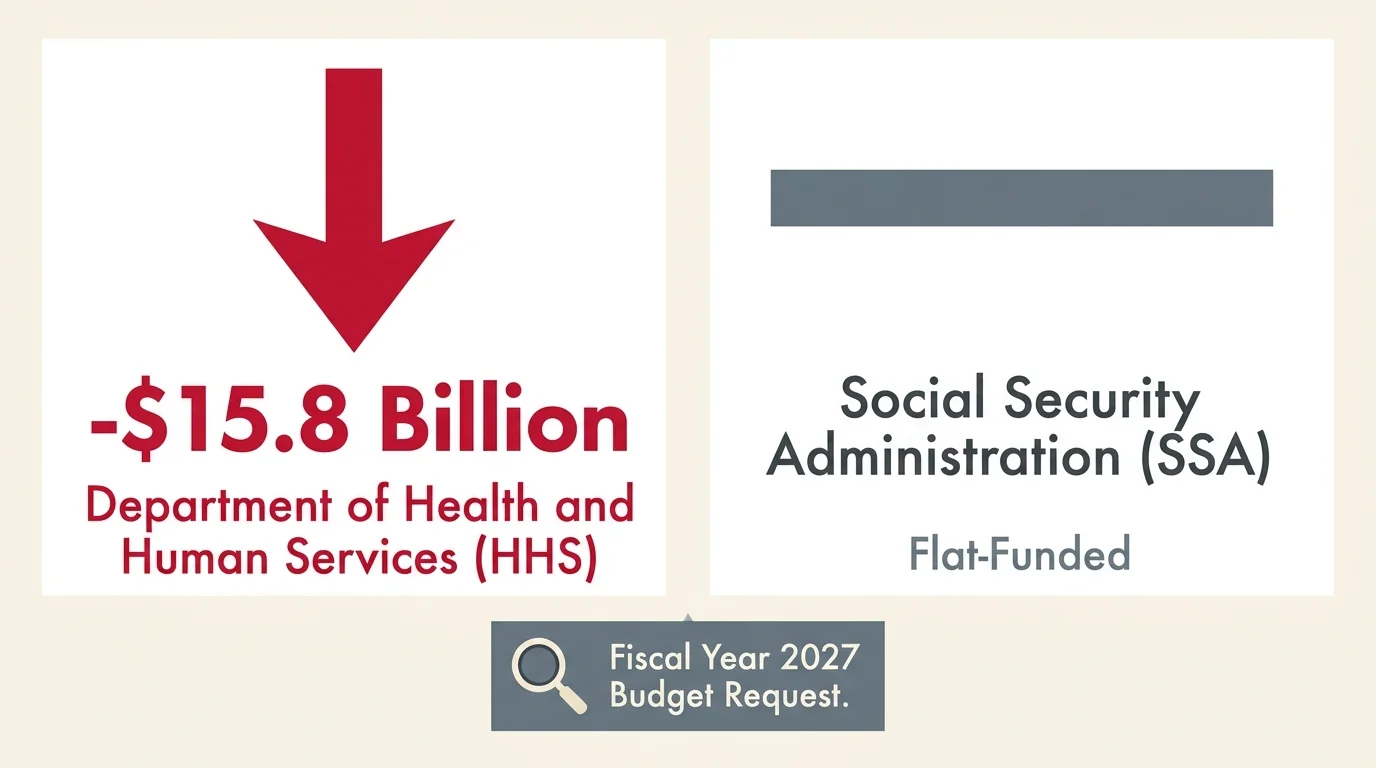

The administration released its Fiscal Year 2027 budget request in April 2026, delivering a stark blueprint that aggressively reshapes federal health and retirement spending. You are currently watching a massive ideological collision in Washington over how the government funds your most critical safety nets. The White House proposes slashing the Department of Health and Human Services budget by $15.8 billion while flat-funding the administrative operations of the Social Security Administration. Simultaneously, lawmakers are fiercely debating new structural limits to entitlement programs that could alter the financial trajectory of millions of older Americans.

As you navigate the economic realities of 2026, you face a frustrating paradox. The Social Security Administration granted a 2.8 percent cost-of-living adjustment this January, lifting the average retirement check to $2,071. Yet rising Medicare premiums and persistent inflation threaten to wipe out that modest gain before the money even reaches your bank account. This new budget cycle is not just a routine bureaucratic exercise; it is a fundamental renegotiation of the American retirement contract. With the October 1 fiscal deadline looming and midterm elections accelerating the political rhetoric, the decisions made in the congressional markup rooms over the next few months will dictate the quality and accessibility of the benefits you earned over a lifetime of labor.

The Power Players and Campaign Strategies Shaping Your Benefits

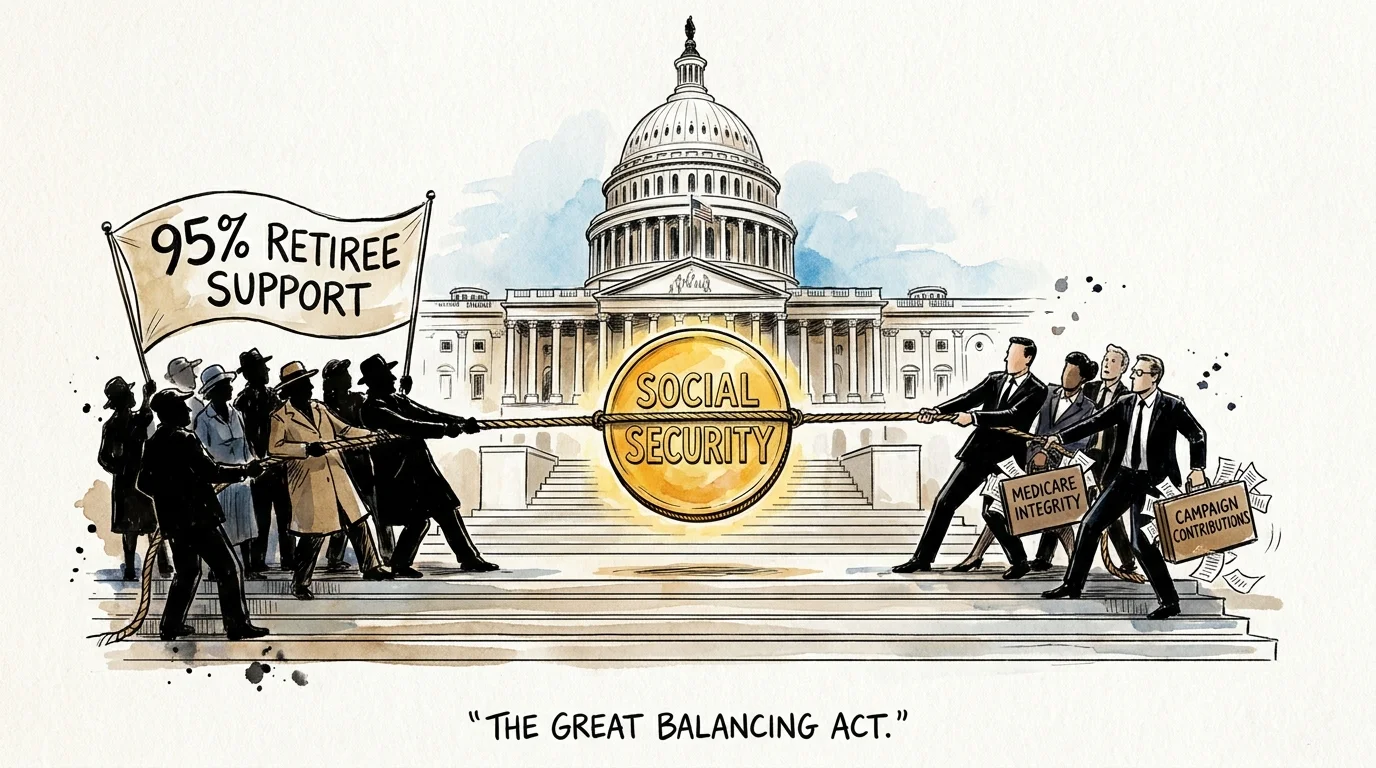

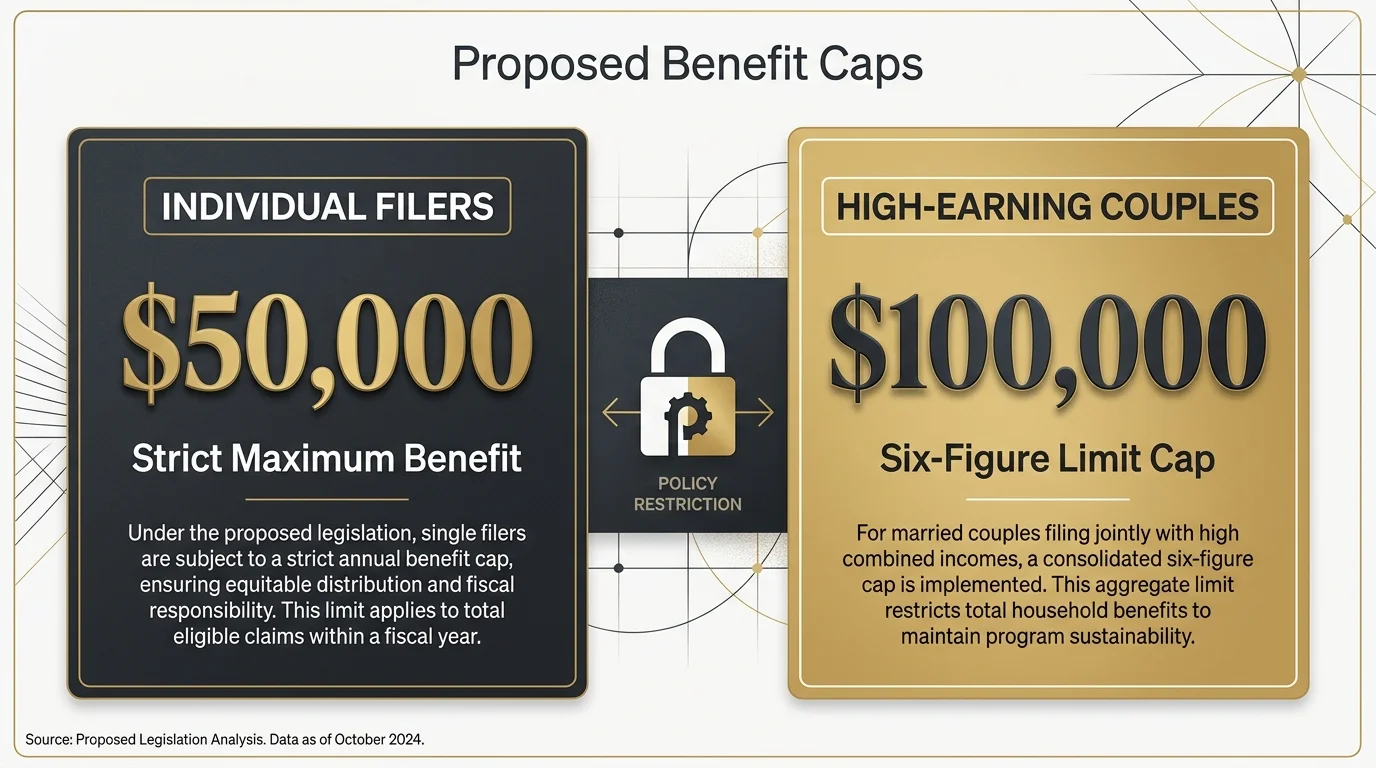

When you look past the public hearings, the real battle over your retirement benefits is playing out among deep-pocketed lobbying coalitions, grassroots advocacy groups, and think tanks pushing radical reforms. The Committee for a Responsible Federal Budget recently jolted the policy landscape by proposing a Six-Figure Limit on Social Security, which would cap maximum retirement benefits for high-earning couples at $100,000 annually. Fiscal conservatives argue this cap is a mathematical necessity to rescue a trust fund projected to face insolvency by 2032. If enacted, individual filers at full retirement age would see a strict maximum benefit of $50,000 per year.

On the other side of the battlefield, entrenched advocacy juggernauts are mobilizing millions of older voters to block any structural cuts. These grassroots groups wield massive electoral influence, frequently citing internal polling that shows 95 percent of retirees fundamentally oppose any benefit reductions. They are aggressively lobbying vulnerable members of the House Ways and Means Committee, demanding that lawmakers protect current payout structures at all costs.

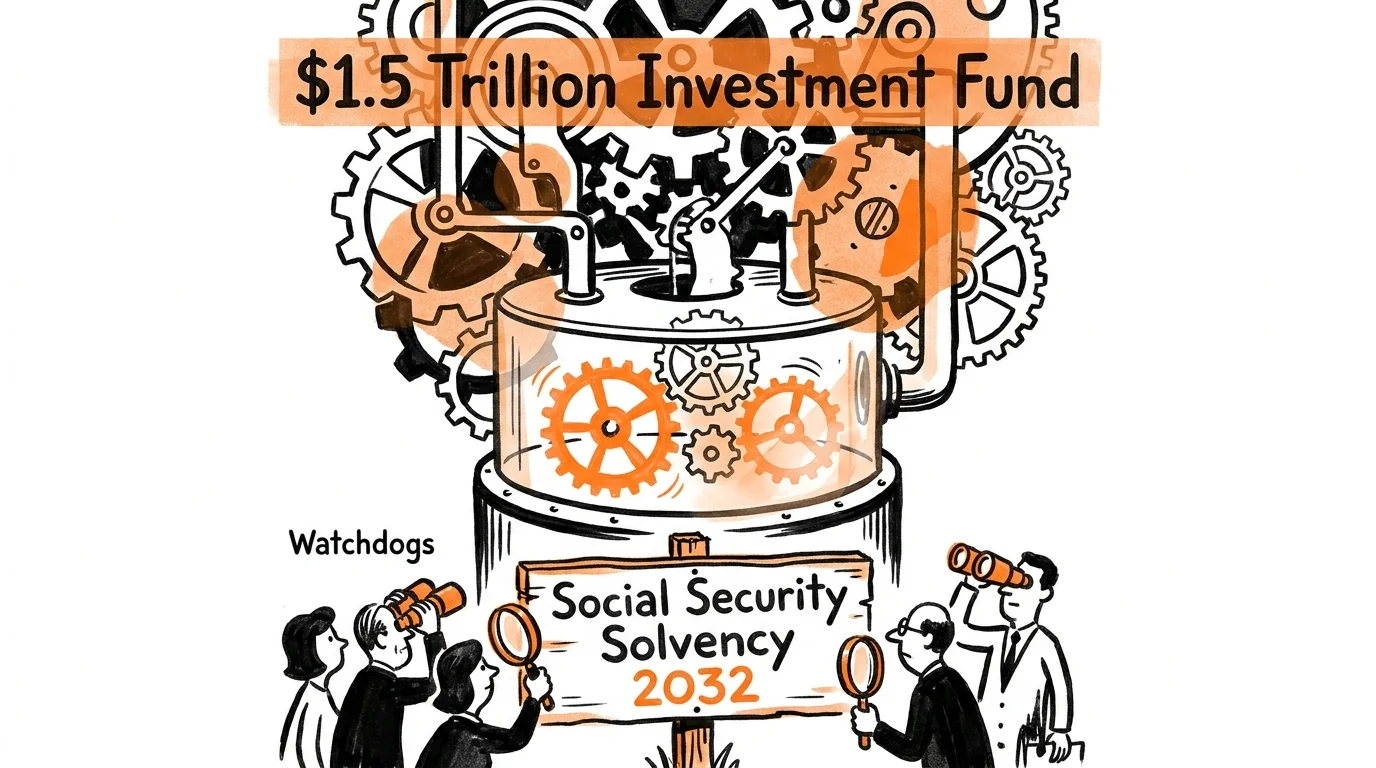

Meanwhile, a parallel power struggle is raging over the Medicare apparatus. Pharmaceutical companies and hospital networks are funneling millions of dollars in campaign contributions into the coffers of key appropriators. Federal Election Commission filings reveal a surge of industry cash aimed at ensuring the administration’s proposed $2.8 billion boost to Medicare and Medicaid program integrity targets bureaucratic waste rather than cutting provider reimbursements. Lawmakers are attempting to thread the needle between these warring factions. Senator Bill Cassidy, for instance, is floating an independent $1.5 trillion investment fund designed to generate high-yield market returns to cover future Social Security shortfalls without triggering immediate payroll tax hikes. As these entities clash, your financial security hangs in the balance of their negotiated compromises.

Decoding the Budget Statutes and Administrative Rules

To understand how the federal budget affects your daily life, you must decode the dense statutory language buried within the administration’s requests. The most glaring number in the April 2026 release is the 12.5 percent reduction to discretionary funding for the Department of Health and Human Services. This sweeping cut includes a proposed $484 million reduction for the Centers for Disease Control and Prevention and a 10 percent cut to the National Institutes of Health.

The budget also signals a profound structural reorganization. The administration wants to consolidate several public health operations into a new entity dubbed the Administration for a Healthy America, moving the 340B Drug Pricing Program directly under the Centers for Medicare and Medicaid Services. While the administration claims this move will streamline operations and battle chronic disease, you should view this centralization of regulatory power with skepticism. Consolidating these massive programs often leads to administrative bottlenecks that delay your access to discounted medications.

Furthermore, the Centers for Medicare and Medicaid Services is slated to receive $3.7 billion to modernize its administrative technology, launching ClaimsCore, an artificial intelligence-driven claims system. Upgrading old technology sounds beneficial on the surface; however, the introduction of artificial intelligence into health insurance networks carries immense risks of automated medical denials. The Older Americans Act also faces severe headwinds under this budget blueprint. The proposal recommends entirely eliminating the Title V Senior Community Service Employment Program, which provides critical part-time work for low-income seniors. Even highly specialized support networks are on the chopping block. The budget slashes the Alzheimer’s Disease Program by 46.6 percent, removing $14.7 million that would otherwise fund dementia-capable services in your local community.

How the Federal Spending Shifts Hit Your Wallet

The abstract numbers debated in Washington translate into very concrete financial realities for your household. The federal government allocates roughly 62 percent of its age-assignable spending—about $2.7 trillion—directly to retirees through Social Security, Medicare, and related benefits. When lawmakers alter these formulas, the shockwaves hit your checkbook immediately.

Consider the math surrounding the 2026 cost-of-living adjustment. The 2.8 percent increase bumped the average monthly Social Security retirement check by about $56. That modest raise should provide a buffer against inflation. However, the federal government simultaneously increased the standard Medicare Part B premium to $202.90 per month. Because the government deducts this premium directly from your Social Security payment, the healthcare cost hike cannibalizes a massive portion of your raise. Once you factor in the rising Part B annual deductible, which now sits at $283, your actual purchasing power remains entirely stagnant.

The demographic and regional impacts of the proposed FY 2027 budget are even more severe. If you live in a rural area or a state that relies heavily on federal block grants to fund local aging infrastructure, the flat-funding of the Older Americans Act will force immediate service reductions. Local governments will have to scale back Meals on Wheels deliveries and reduce the operating hours of community senior centers. If you are a lower-income senior relying on the Senior Community Service Employment Program to pay for basic groceries, the complete elimination of that initiative threatens to push you entirely out of the workforce.

On a slightly positive note, a new federal tax deduction for individuals 65 and older takes effect for the 2025 tax year, which you will file in 2026. This deduction allows eligible seniors to reduce their taxable income, potentially shielding a larger portion of your Social Security benefits from federal taxes. However, the benefit phases out for retirees with a modified adjusted gross income over $75,000, meaning middle-class seniors will see the most relief while higher earners receive virtually no protection.

Watchdog Concerns Over Transparency and Privatization

Whenever the federal government proposes massive shifts in health care spending, ethical concerns and oversight challenges immediately follow. The administration intends to inject $2.8 billion into the Health Care Fraud and Abuse Control program and Medicaid Integrity programs. While preventing the theft of taxpayer dollars is a universally supported goal, the mechanics of how the government pursues this fraud require intense scrutiny. Independent watchdog organizations frequently warn that federal anti-fraud contractors operate under perverse incentives. Because these auditors often recover funds on a contingency basis, they are financially motivated to harass independent physicians over minor billing technicalities rather than dedicating resources to dismantle sophisticated, large-scale criminal fraud rings. This aggressive regulatory environment causes many local doctors to stop accepting Medicare patients entirely, directly limiting your access to quality medical care.

Transparency advocates are also sounding the alarm over the technological overhaul at the Centers for Medicare and Medicaid Services. The implementation of the artificial intelligence-driven ClaimsCore system lacks robust public oversight. Algorithms designed to detect billing anomalies can easily be calibrated to automatically deny legitimate medical claims, forcing you to navigate a labyrinthine appeals process just to get your basic treatments covered. Lawmakers have yet to establish clear legislative guardrails ensuring that human doctors, rather than opaque software programs, have the final say on your medical necessity.

Election finance trackers are monitoring a flood of dark money advertisements supporting the creation of the new Administration for a Healthy America. These political action committees actively shield the identities of corporate donors who stand to profit from the privatization of federal health initiatives. Whenever administrative functions are outsourced or consolidated, private contractors swoop in to secure lucrative federal contracts. As a constituent, you must demand that your representatives force the administration to publish transparent performance metrics for these new contractors, ensuring that your tax dollars fund actual patient care rather than corporate profit margins.

Answers to Your Critical Budget Questions

When will the proposed federal budget changes actually take effect?

The proposals outlined in the April 2026 budget request are designed for Fiscal Year 2027, which officially begins on October 1, 2026. However, presidential budgets serve primarily as policy blueprints rather than binding legislation. Congress holds the power of the purse and must draft, debate, and pass the actual appropriations bills. If lawmakers fail to reach a comprehensive agreement by the autumn deadline, they will likely rely on short-term continuing resolutions. These stopgap measures would temporarily maintain current funding levels and delay any major programmatic overhauls until after the balance of power is decided in the upcoming November elections.

Will the proposed Six-Figure Limit reduce your current Social Security benefits?

If you are currently receiving Social Security, the proposed Six-Figure Limit is highly unlikely to reduce your existing monthly checks. This framework, championed by fiscal conservatives to address the looming trust fund shortfall, specifically targets future beneficiaries who would theoretically claim the highest possible benefits at full retirement age. Lawmakers across the political spectrum are notoriously hesitant to touch the guaranteed benefits of current retirees, knowing that older Americans participate in elections at staggering rates. Furthermore, the limit is currently just a think-tank proposal and must overcome massive legislative hurdles before it could ever become binding law.

How do rising Medicare Part B premiums impact your net monthly income?

Your net Social Security income is the exact amount deposited into your bank account after all mandatory federal deductions. For 2026, the Centers for Medicare and Medicaid Services increased the standard Part B premium to $202.90 per month. Because the federal government automatically deducts this health insurance premium from your Social Security benefits, the hike consumes a significant portion of your recent 2.8 percent cost-of-living adjustment. Even though your gross benefit may have increased by an average of $56 per month, the higher premium means your actual take-home pay might only increase by a few dollars, severely limiting your ability to absorb broader economic inflation.

What happens to essential retiree services if Congress fails to pass a budget?

A failure to pass a comprehensive budget by the October 1 deadline forces the government to rely on continuing resolutions, which freeze federal spending at previous historical levels. During a continuing resolution, federal agencies cannot launch new policy initiatives or adjust their spending to meet current inflationary demands. If the political stalemate devolves into a full government shutdown, core entitlement programs like Medicare and Social Security will continue to issue your monthly payments because they rely on permanent, mandatory funding. However, discretionary grants that fund local senior centers, administrative offices processing new benefit claims, and community-based employment programs would face immediate suspension, disrupting the localized safety nets you rely on every day.

The Next Legislative Milestones You Must Monitor

The release of the April 2026 budget blueprint is merely the opening salvo in a grueling legislative war. As the summer approaches, you must closely monitor the markup sessions within the House and Senate Appropriations Committees. These closed-door meetings are where lawmakers will either rubber-stamp the administration’s deep cuts to the Department of Health and Human Services or aggressively restore funding to essential programs like the Older Americans Act.

Pay immediate attention to how Congress addresses the impending Social Security trust fund shortfall. While the $1.5 trillion investment fund and the Six-Figure Limit dominate the current think-tank discussions, legislative action will require significant bipartisan compromise before the end of the year. Additionally, watch the actions surrounding the Medicare physician fee schedule. If Congress fails to pass stabilization acts to protect provider reimbursements, your local doctors may be forced to limit the number of Medicare patients they accept. The ultimate fate of your retirement benefits will be decided in the chaotic weeks leading up to the October 1 fiscal deadline. Stay engaged, review your lawmakers’ voting records, and prepare your household budget for a volatile year of federal policy shifts.