As Congress wrestles with mounting federal deficits and impending trust fund shortfalls, the rules governing your retirement are quietly undergoing their most significant rewrite in a generation. From overhauled prescription drug caps to shifting tax liabilities on your monthly benefits, these government updates directly dictate how much money stays in your pocket this year. Navigating this shifting landscape requires cutting through partisan noise to understand exactly what lawmakers are deciding behind closed doors. This year brings eight critical policy decisions that will reshape your healthcare costs, your investment protections, and your baseline income. By examining the raw legislative data and the latest agency directives, you can anticipate these changes and protect the financial security you spent a lifetime building.

Background and Timeline: How We Got Here

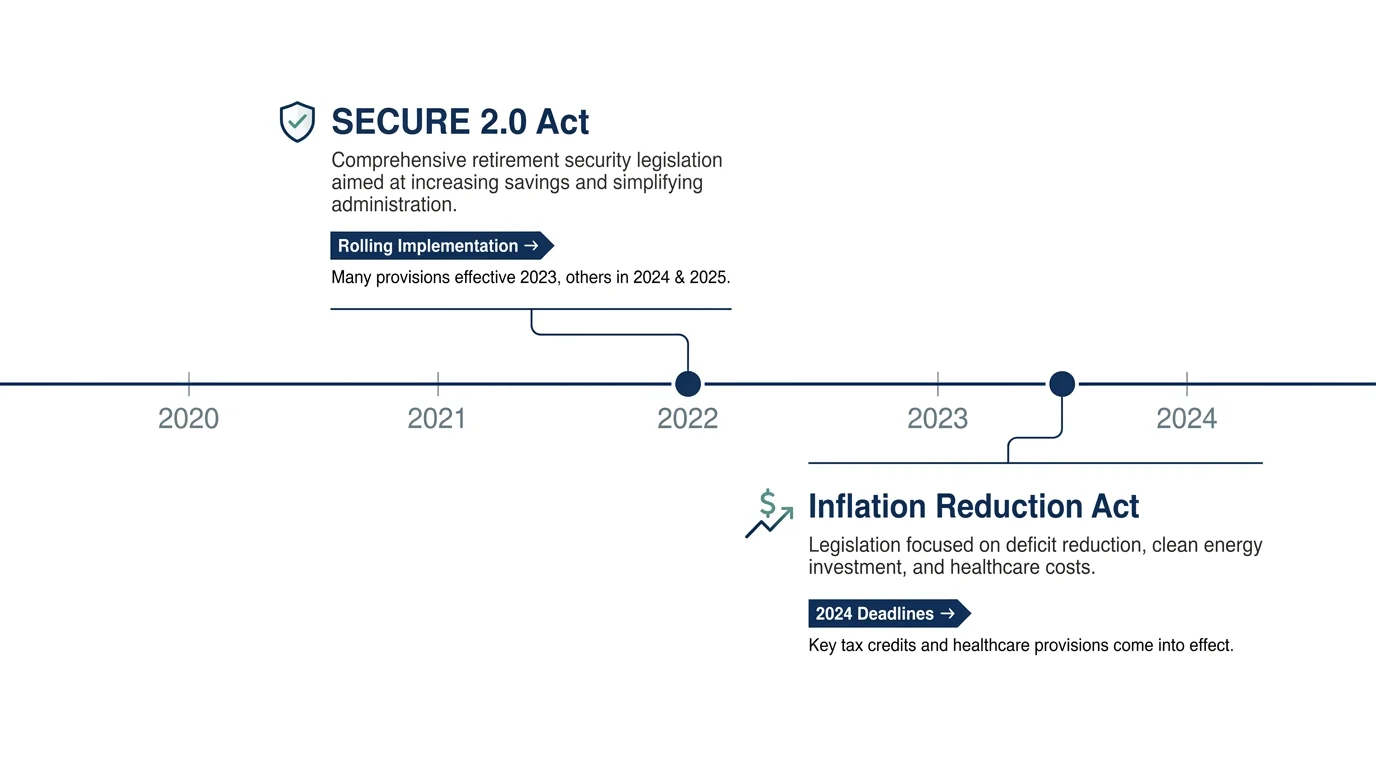

The foundation for this year’s most consequential retirement policies was poured over the last four years. Following the economic volatility of the early 2020s, lawmakers enacted two sweeping pieces of legislation: the SECURE 2.0 Act and the Inflation Reduction Act. Both bills bypassed immediate, sweeping changes in favor of staggered implementations that are only now reaching your wallet. The delayed start dates were designed to give federal agencies and the financial industry time to adjust, but they also created a complex web of rolling deadlines that you must now navigate.

Simultaneously, the structural integrity of the nation’s safety net remains a pressing issue on Capitol Hill. According to recent Congressional Budget Office projections, the primary Social Security trust fund will face depletion early in the next decade if lawmakers fail to act. This impending deadline acts as an invisible hand guiding current policy debates. Every adjustment to cost-of-living formulas, healthcare subsidies, and tax thresholds is now weighed against the broader solvency of the federal retirement system.

Core Analysis: The Eight Critical Policy Changes

1. The Social Security Cost-of-Living Adjustment Formula

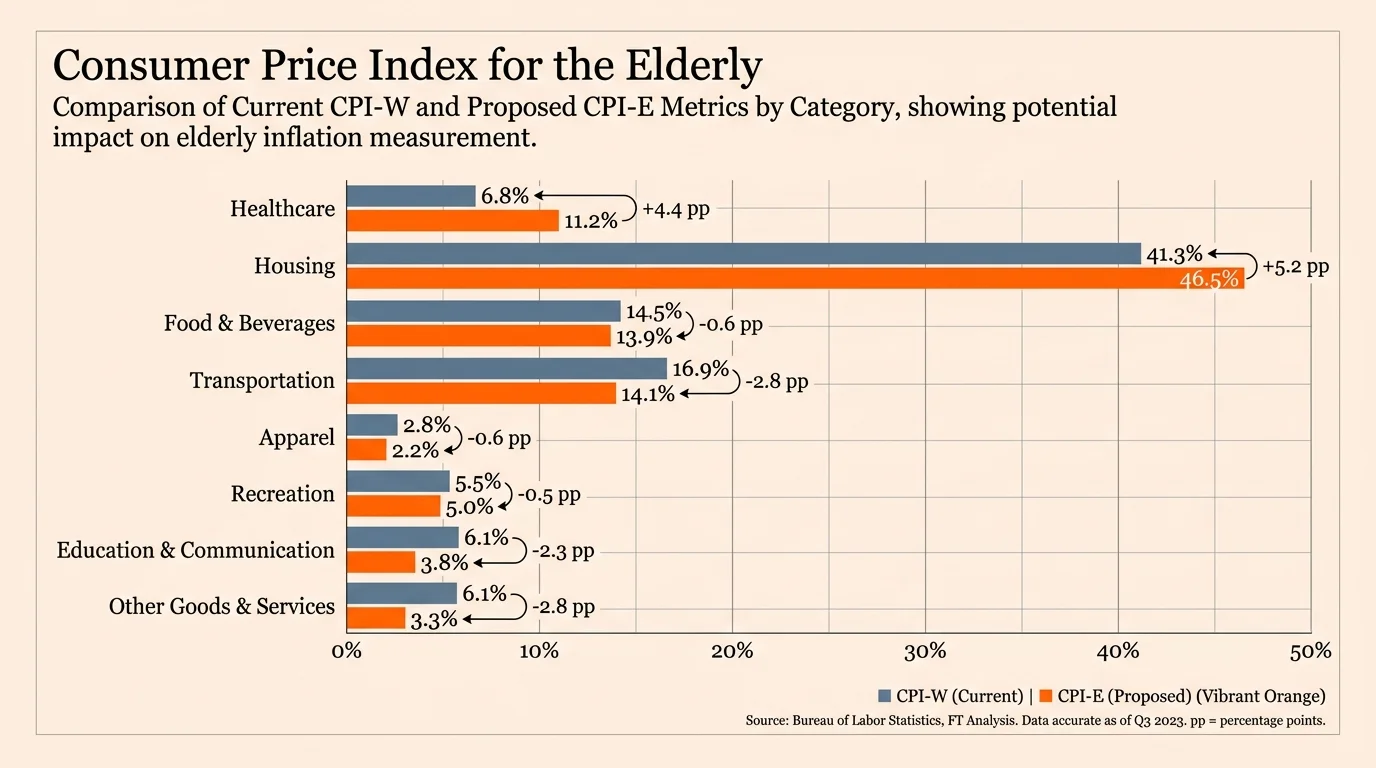

The annual cost-of-living adjustment determines whether your Social Security check keeps pace with inflation. Currently, the Social Security Administration calculates this increase using the Consumer Price Index for Urban Wage Earners and Clerical Workers. Policy analysts widely acknowledge that this metric tracks the spending habits of younger, working-age populations, heavily weighting costs like transportation and apparel. Lawmakers are currently debating a shift to the Consumer Price Index for the Elderly, a metric that places a much heavier emphasis on housing and healthcare—the two sectors where you likely spend the majority of your income. Adopting this new formula would permanently alter the trajectory of your lifetime benefits.

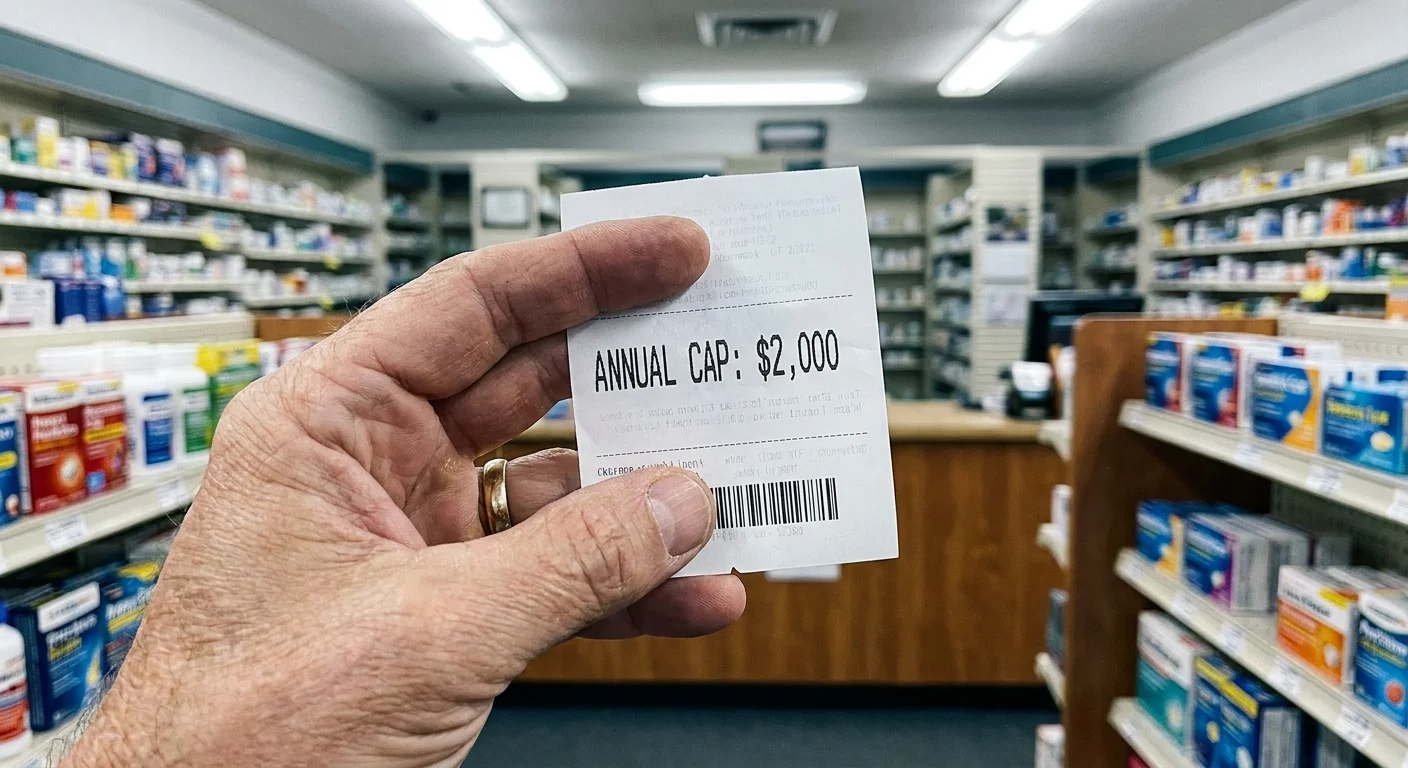

2. Medicare Part D Out-of-Pocket Spending Caps

Your exposure to catastrophic pharmacy costs shifted dramatically following recent updates to Medicare Part D. Thanks to rolling provisions from the Inflation Reduction Act, your out-of-pocket spending for covered prescription drugs is now strictly capped at two thousand dollars annually. Beyond this cap, the newly implemented Medicare Drug Price Negotiation Program is taking full effect. The Centers for Medicare and Medicaid Services implementation guidelines detail how the government will pay lower negotiated prices for several of the most common and expensive blood thinner, diabetes, and heart failure medications. This policy directly reduces the co-insurance obligations you face at the pharmacy counter.

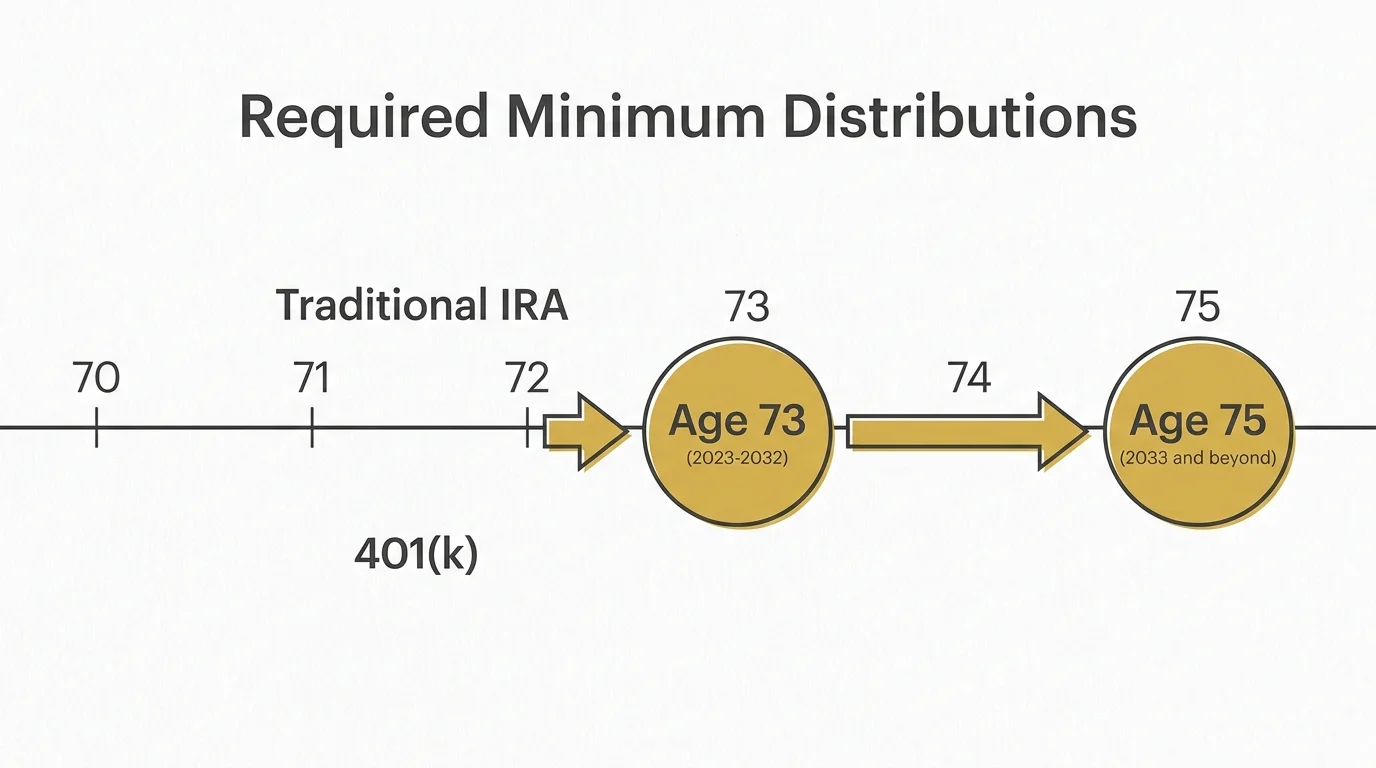

3. SECURE 2.0 Act Required Minimum Distribution Shifts

If you hold a traditional IRA or a 401(k), the IRS mandates that you begin withdrawing a specific amount of money from those accounts each year. Prior to the SECURE 2.0 Act, you had to start taking these Required Minimum Distributions at age 72. Lawmakers recently pushed that age to 73, granting your investments an extra year of tax-deferred growth. Congress is currently drafting guidance for the next scheduled shift, which will push the starting age to 75. Knowing precisely when you must begin withdrawing funds is critical, as failing to take the exact minimum distribution triggers a severe excise tax penalty on the un-withdrawn amount.

4. Medicare Advantage Marketing and Funding Regulations

Federal regulators are fundamentally altering how insurance companies can sell you Medicare Advantage plans. Following widespread reports of deceptive television advertising and high-pressure sales tactics, the government enacted strict limits on broker compensation and banned advertisements that use confusing federal logos. Additionally, lawmakers are scrutinizing the algorithmic software many Medicare Advantage insurers use to deny post-acute care and rehabilitation stays. The new policies force insurers to rely on traditional medical necessity criteria rather than proprietary computer models, ensuring you receive the coverage promised during the enrollment period.

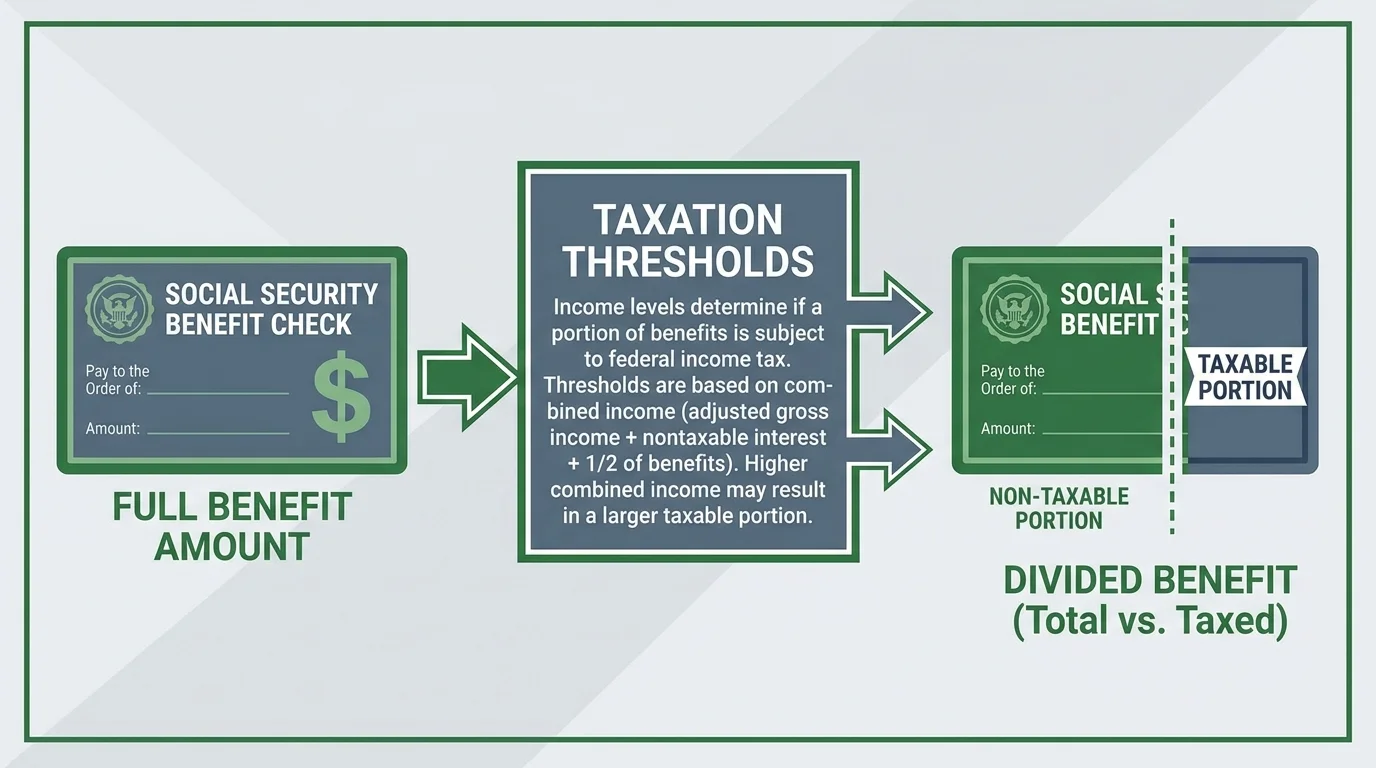

5. Taxation Thresholds for Social Security Benefits

A growing number of seniors are shocked to discover that the IRS taxes a portion of their Social Security income. Congress established the income thresholds for this tax in the 1980s and 1990s, setting them at twenty-five thousand dollars for an individual and thirty-two thousand dollars for a married couple. Because lawmakers deliberately chose not to index these thresholds to inflation, ordinary cost-of-living adjustments naturally push more retirees over the line each year. Policymakers are currently debating whether to raise these limits or abolish the tax entirely, a decision that would instantly increase the take-home pay for millions of middle-class households.

6. Long-Term Care and Nursing Home Staffing Mandates

The quality of care you or your spouse might receive in a nursing facility relies heavily on adequate staffing. The Centers for Medicare and Medicaid Services recently finalized a rule mandating strict minimum staffing levels for long-term care facilities that accept federal funding. Facilities must now provide a minimum of three point four eight hours of nursing care per resident, per day. While patient advocacy groups praise the policy for improving safety and reducing neglect, industry operators argue that a severe labor shortage will force facilities to close their doors. You will need to monitor how this policy impacts facility availability in your specific region.

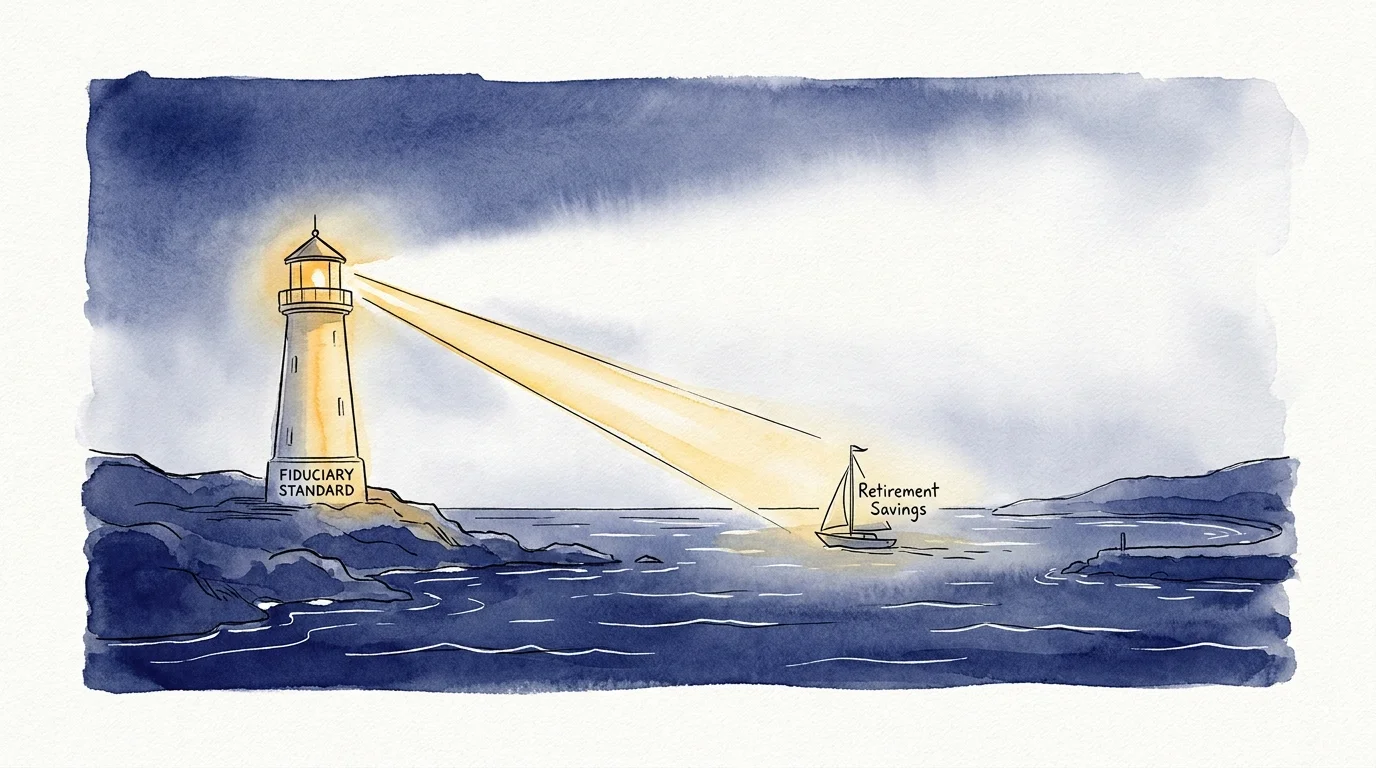

7. Fiduciary Standards for Retirement Advisors

When you roll over a lifelong pension or a 401(k) into a private annuity or IRA, the financial advice you receive dictates the security of your savings. The Department of Labor recently introduced a stringent Retirement Security Rule designed to close loopholes that allowed some advisors to recommend high-commission products that were not in their clients’ best interests. By expanding the definition of an investment advice fiduciary, the rule forces brokers to prioritize your financial well-being over their own profit margins. Legal battles mounted by the insurance industry currently threaten to block this policy, leaving the standard of care you receive hanging in the balance.

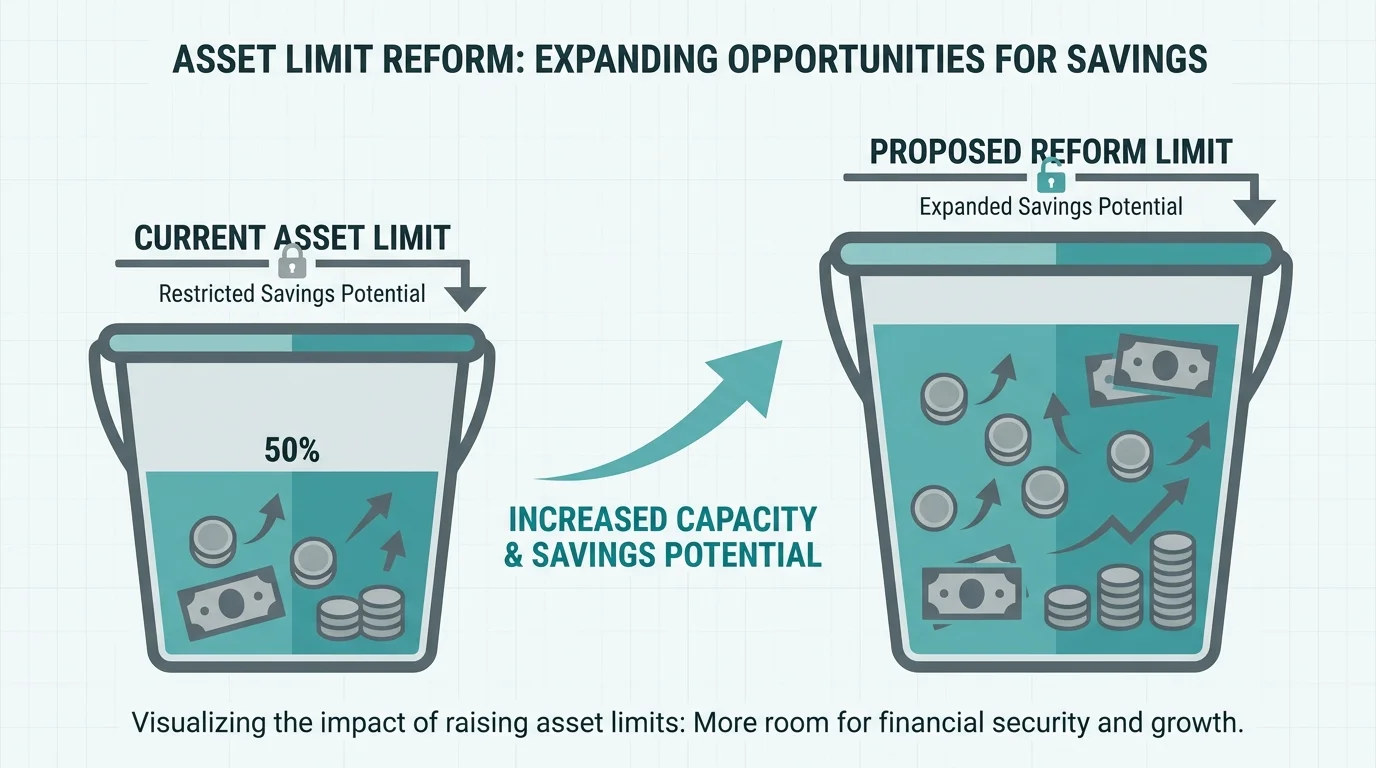

8. Supplemental Security Income Asset Limit Reforms

Supplemental Security Income provides a vital safety net for the nation’s most impoverished seniors, but the program enforces exceptionally strict asset limits. Currently, you lose eligibility if you hold more than two thousand dollars in total assets—a threshold Congress has not updated since 1989. Bipartisan legislation is advancing to raise this limit to ten thousand dollars for individuals. According to Bipartisan Policy Center analysis, modernizing this policy would allow vulnerable seniors to maintain a modest emergency savings account without fear of losing their basic subsistence and healthcare coverage.

Impact Lens: Economic and Community Consequences

These eight policy shifts do not operate in a vacuum; they interact to reshape your monthly budget and your long-term financial security. Consider how the unindexed tax thresholds conflict with your annual cost-of-living adjustments. When your Social Security check increases to match inflation at the grocery store, that same increase might tip your total income over the twenty-five thousand dollar mark. Suddenly, the IRS taxes a portion of your benefits, meaning your net income actually decreases despite the inflation adjustment.

The real-world consequences of these policy interactions are visible in communities across the country. In rural areas, the new nursing home staffing mandates force families to weigh the benefit of improved care quality against the very real risk of their local facility shutting down due to an inability to hire registered nurses. Conversely, the out-of-pocket caps on Medicare Part D act as an immediate economic stimulus for households previously burdened by chronic illness. By limiting pharmacy spending, lawmakers free up capital that seniors can redirect toward housing, food, and local services. Understanding the interplay between these policies allows you to adjust your withdrawal strategies and healthcare selections before the government finalizes the rules.

Accountability Check: Oversight and Transparency Gaps

While the federal government heavily promotes the benefits of these new policies, significant blind spots remain regarding how agencies enforce them. The complex bureaucracy surrounding Medicare Advantage presents one of the most pressing accountability failures. Despite new marketing regulations, the government struggles to track exactly how much taxpayer money flows into the administrative overhead of private insurance giants. Government Accountability Office investigations frequently reveal that Medicare Advantage plans routinely overcharge the government by billions of dollars through aggressive diagnostic coding.

Similarly, transparency remains poor within the prescription drug supply chain. Although lawmakers capped your out-of-pocket costs, Pharmacy Benefit Managers continue to negotiate secretive rebate deals with drug manufacturers behind closed doors. These opaque practices artificially inflate the initial list prices of medications, driving up the baseline premiums you pay every month for your Medicare Part D coverage. Congress continues to hold hearings demanding greater visibility into these corporate practices, but the legislative remedies often lack the enforcement mechanisms necessary to compel true pricing transparency.

Frequently Asked Questions

How do these legislative shifts affect existing retirement accounts?

Changes to Required Minimum Distributions and fiduciary rules apply to both new and established retirement accounts. If you already began taking minimum distributions under the old age rules, you must continue your current withdrawal schedule. However, if you have not yet reached the new age thresholds, you benefit from the extended tax-deferral period regardless of when you originally opened your traditional IRA or 401(k).

Can executive agencies alter Medicare rules without a congressional vote?

Yes. Congress delegates broad authority to the Centers for Medicare and Medicaid Services to interpret and execute existing health laws. This means the agency can unilaterally change the rules governing Medicare Advantage marketing, broker compensation, and nursing home staffing standards through the federal rulemaking process. These regulatory updates carry the full weight of the law without requiring a new vote in the House or Senate.

What precedent exists for taxing Social Security benefits?

Lawmakers first introduced taxes on Social Security benefits in 1984 to help shore up the program’s trust fund, taxing up to fifty percent of benefits for higher earners. In 1993, Congress expanded the policy to tax up to eighty-five percent of benefits for an additional tier of earners. Because lawmakers explicitly designed the legislation without automatic inflation adjustments, the tax now captures millions of middle-income retirees that the original policy never intended to target.

How quickly will the new nursing home mandates take effect?

The federal government utilizes a staggered, multi-year phase-in strategy for the new staffing rules to prevent immediate facility closures. Urban facilities generally have three years to fully comply with the registered nurse coverage requirements, while rural facilities receive up to five years. Regulators built in temporary hardship exemptions for facilities operating in regions with documented, severe workforce shortages.

Forward Look: Upcoming Deadlines and Election Stakes

The policies shaping your retirement remain highly fluid as the calendar pushes toward the end of the year. Lawmakers return to Washington this winter facing intense pressure to fund the government and address several expiring healthcare provisions during the lame-duck legislative session. Your immediate focus must turn to the Medicare open enrollment period, which dictates your premium costs and pharmacy coverage for the entire upcoming calendar year. Insurance companies heavily restructured their plan offerings to absorb the new out-of-pocket drug caps, meaning the plan that served you well last year may no longer be your most cost-effective option.

Beyond healthcare, the impending expiration of the Tax Cuts and Jobs Act casts a massive shadow over your long-term financial planning. According to Tax Foundation research, if Congress allows these tax provisions to sunset at the end of next year, the standard deduction will drop significantly. This automatic tax increase would force millions of retirees to resume itemizing deductions to protect their fixed incomes. The upcoming elections will decide exactly which lawmakers hold the pen when the time comes to rewrite these fundamental financial rules.