The Flashpoint: A Summer of Budget Battles and Campaign Promises

During a tense House Ways and Means Committee hearing earlier this spring, lawmakers abandoned polite oversight to launch direct partisan attacks over the approaching insolvency of federal retirement programs. The stakes extend far beyond the mahogany desks of Capitol Hill committee rooms; this clash signaled the unofficial start of the 2026 midterm messaging war. With control of both the House and the Senate hanging by threadbare margins, politicians from both sides of the aisle are weaponizing the future of your retirement to secure electoral victories. The hearing featured fierce debates over actuarial projections and spending caps, immediately spawning a wave of super PAC television advertisements across swing states.

You are witnessing a deliberate political calculation unfold in real time. Candidates recognize that older Americans consistently vote at the highest rates of any demographic group. Therefore, any perceived threat to earned benefits serves as the ultimate political motivator. Incumbents face intense pressure to demonstrate their commitment to protecting these safety nets, while challengers eagerly highlight past votes or budget proposals to paint their opponents as threats to financial stability. This dynamic transforms complex fiscal policy into rapid-fire campaign slogans, often obscuring the genuine mathematical crises facing these essential government programs.

The legislative reality remains stark and unavoidable. Lawmakers face a rapidly closing window to enact meaningful reforms before mandatory, across-the-board benefit cuts trigger automatically in the next decade. This impending deadline forces every candidate running in the 2026 midterms to formulate a coherent position on taxes, spending, and entitlement reform. The promises they make on the campaign trail today will directly dictate the legislative agenda of the next Congress—and ultimately decide the financial trajectory of your retirement years.

Players and Strategy: Mapping the Influence Network

Understanding the future of your benefits requires tracking the intricate web of influence driving the legislative process. AARP remains the undisputed heavyweight in this arena. Operating with a massive membership base and unparalleled lobbying resources, the organization mobilizes voters with surgical precision. Their strategists deploy aggressive mail campaigns and digital advertising to pressure candidates into signing public pledges against benefit reductions. When AARP issues a legislative alert, switchboards on Capitol Hill light up, forcing lawmakers to immediately justify their policy positions to a highly engaged constituency.

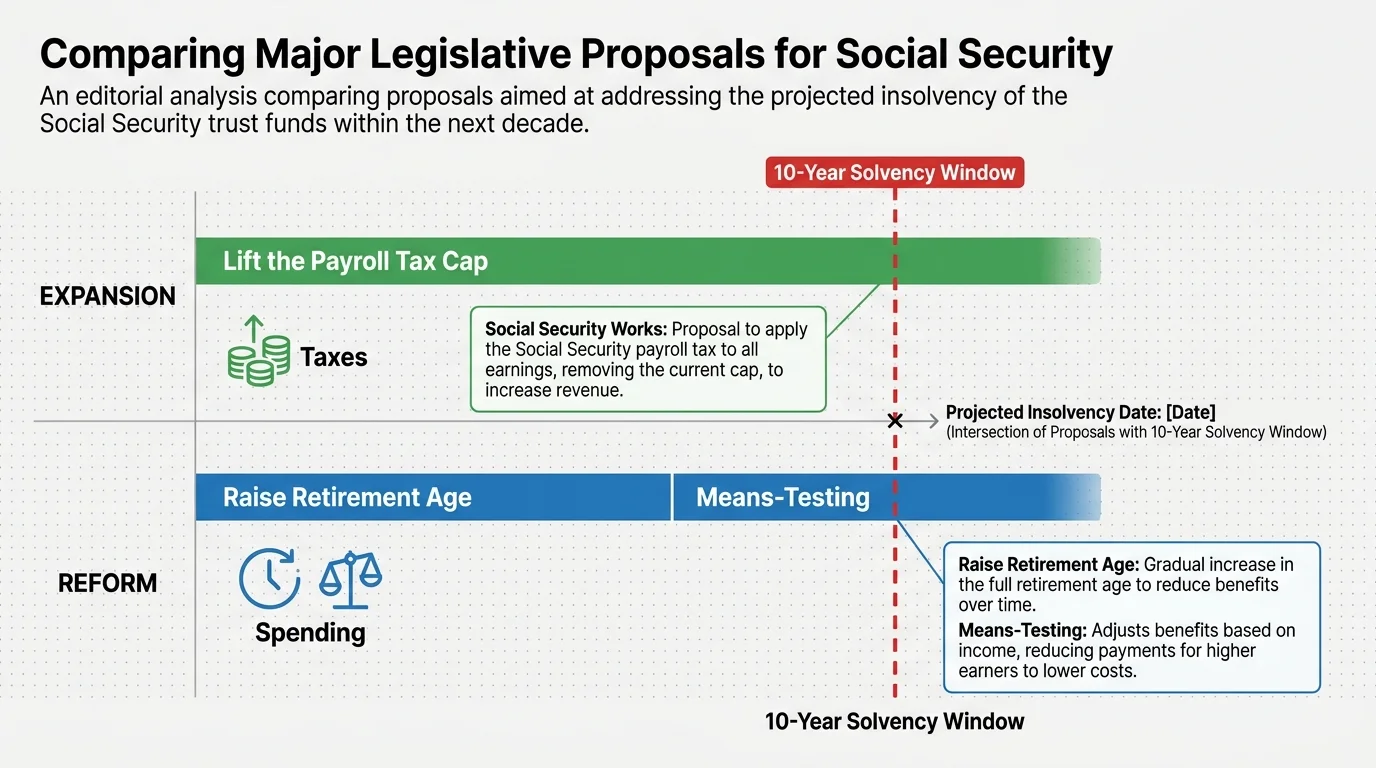

Counterbalancing the advocacy groups are well-funded fiscal conservative think tanks and business roundtables. These organizations argue that without immediate structural adjustments, the growing national debt will trigger an unprecedented economic crisis. They actively recruit and fund primary challengers who are willing to champion unpopular but—in their view—necessary reforms, such as raising the retirement age or implementing means-testing for wealthier retirees. An analysis of Federal Election Commission filings reveals these groups are funneling tens of millions of dollars into key battleground districts, particularly in states like Pennsylvania, Michigan, and Arizona.

Progressive advocacy networks operate with equal intensity on the opposite side of the ledger. Groups like Social Security Works demand expansion of benefits and advocate for lifting the payroll tax cap entirely, ensuring that the wealthiest earners pay into the system on all of their income. They coordinate closely with organized labor and progressive caucuses to frame any discussion of benefit cuts as a direct assault on the working class. You will see these competing factions dominating your local airwaves over the coming months; they carefully tailor their messaging to exploit economic anxieties and drive distinct voter bases to the polls.

Policy Breakdown: Decoding the Legislative Proposals

Political rhetoric frequently masks the specific, technical mechanisms lawmakers intend to use to alter your benefits. You must cut through the campaign jargon to understand exactly what is on the negotiating table. One of the primary proposals circulating in budgetary discussions involves raising the full retirement age. Currently set at 67 for anyone born in 1960 or later, fiscal hawks propose gradually increasing this threshold to 69 or even 70. If Congress implements this change, you face a significant reduction in your lifetime benefit payout unless you remain in the workforce for several additional years.

Another highly debated concept is the implementation of a chained Consumer Price Index to calculate annual cost-of-living adjustments. Proponents market this as a minor technical correction to inflation tracking, arguing that consumers naturally substitute cheaper goods when prices rise. However, the mathematical reality for your wallet is profound. If lawmakers adopt a chained CPI metric, you will receive systematically smaller annual increases in your monthly checks. Over a decade of retirement, this compounding effect strips thousands of dollars of purchasing power away from individuals living on fixed incomes.

The debate surrounding healthcare proves equally complex and contentious. Traditional coverage and Medicare Advantage plans face rigorous scrutiny as healthcare costs continue to outpace inflation. Some legislative blueprints suggest means-testing traditional Medicare, which would require retirees with higher lifelong earnings to pay significantly larger premiums for their Part B and Part D coverage. Simultaneously, lawmakers are battling over the payment formulas governing Medicare Advantage. Reductions in these federal subsidies could force private insurers to scale back the supplemental dental, vision, and fitness benefits that millions of seniors currently rely upon.

To grasp the full scope of these proposals, you must look beyond partisan summaries. Independent analysts at the Congressional Budget Office continuously model the long-term impact of these specific policy levers. Their reports confirm that bridging the projected funding gaps requires either substantial tax increases, severe benefit reductions, or a carefully engineered combination of both. The candidates you elect in 2026 will possess the legislative authority to choose exactly which demographic bears the brunt of that financial burden.

Constituent Impact: How Your Retirement Could Change

Federal policy shifts rarely distribute their economic consequences evenly; the impact on your household depends heavily on your geographic location, your lifelong earnings, and your health status. In Sunbelt states like Florida and Arizona, where retirees make up a disproportionate percentage of the overall population, any reduction in federal benefits threatens to destabilize entire local economies. If millions of seniors suddenly experience a reduction in their disposable income, the secondary effects immediately hit local retail sectors, service industries, and municipal tax revenues.

The demographic disparities are equally pronounced. For roughly a quarter of Americans over the age of 65, federal benefits constitute more than ninety percent of their total income. If you belong to this vulnerable group, a transition to a chained CPI or an increase in Medicare premiums represents an immediate threat to your basic standard of living. These individuals simply do not possess the private investment portfolios necessary to absorb a permanent reduction in federal support. The lived reality involves rationing prescription medications, skipping medical appointments, or cutting back on essential household utilities.

Conversely, upper-income retirees face a different set of vulnerabilities tied to the 2026 election outcomes. If the newly elected Congress chooses to resolve the insolvency crisis strictly through revenue generation, high earners will experience substantial tax increases. Proposals to lift the payroll tax cap or introduce wealth taxes on retirement distributions directly target affluent households. Furthermore, aggressive means-testing could drastically increase the out-of-pocket healthcare costs for seniors who planned their retirements based on current premium structures.

Rural constituents face unique geographic risks tied to healthcare policy. Rural hospitals frequently operate on razor-thin financial margins, depending heavily on consistent federal reimbursements to keep their doors open. If Congress attempts to extend the life of the trust funds by lowering provider reimbursement rates, many rural clinics and hospitals will simply cease operations. If you live in an agricultural or remote district, your access to emergency care and specialized medicine depends entirely on how your elected representatives balance the healthcare budget.

Oversight and Ethics: Tracking the Money and Messaging

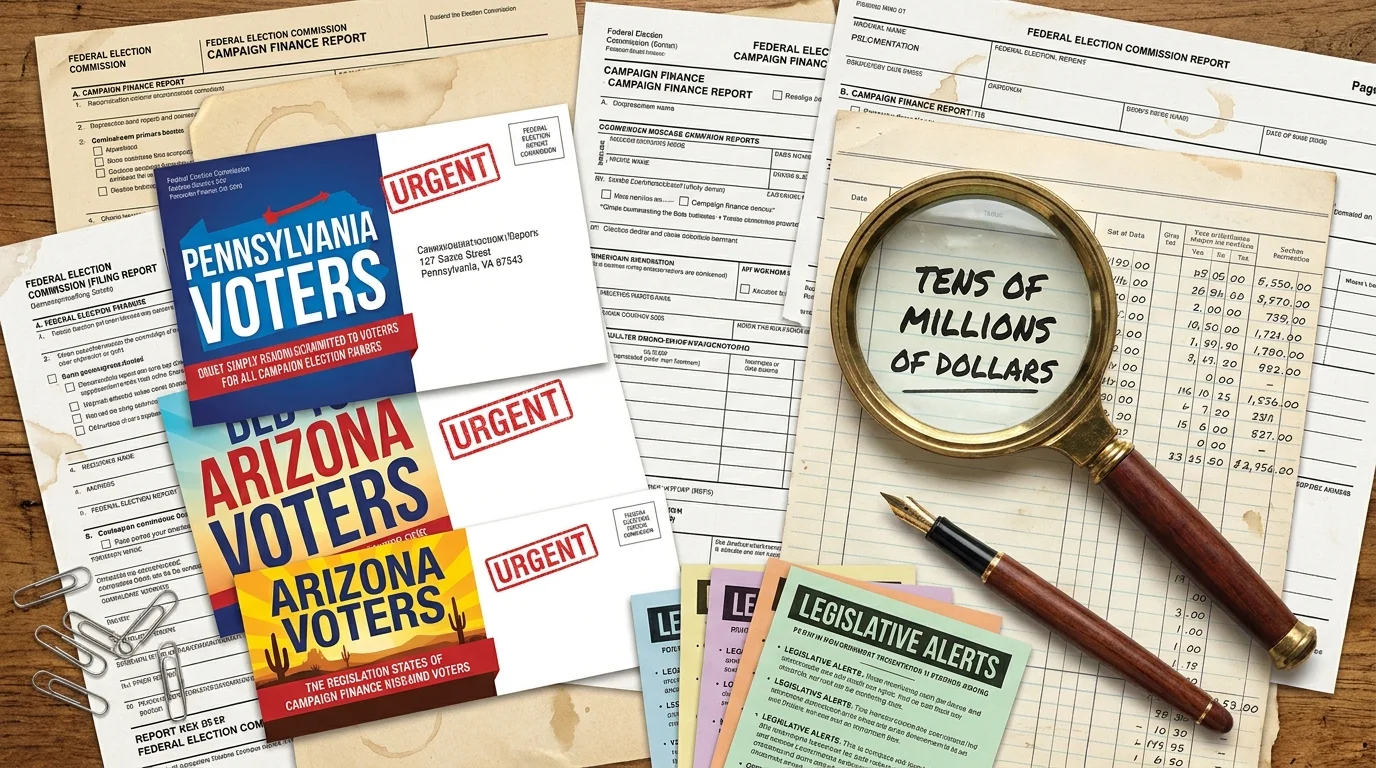

The sheer volume of capital flowing into the 2026 midterm elections creates a fertile environment for dark money and deceptive messaging. As a voter, you must approach political advertisements with a high degree of skepticism. Watchdog organizations note that politically active nonprofits routinely obscure the actual corporate donors and wealthy individuals driving specific policy agendas. These 501(c)(4) organizations buy millions of dollars in broadcast time across crucial media markets; they frame complex actuarial adjustments as either necessary heroic rescues or catastrophic betrayals, depending on their hidden financial interests.

Deceptive campaign tactics frequently target older voters directly through their mailboxes. You often receive mailers designed to mimic the appearance of official government documents—complete with official-looking seals, urgent warning labels, and bureaucratic typography. These are actually carefully engineered political advertisements intended to provoke fear and drive donations. Ethics watchdogs consistently flag these practices, yet federal regulations remain incredibly permissive regarding how political action committees can format their direct mail communications.

Transparency advocates rely on databases like OpenSecrets to trace the flow of lobbying dollars back to the pharmaceutical industry, private insurance conglomerates, and Wall Street investment firms. These corporate entities possess massive financial stakes in how Congress regulates retirement plans and negotiates drug prices. When you observe a sudden, coordinated messaging pivot among multiple candidates regarding privatization or tax restructuring, you are typically watching the direct result of coordinated, behind-the-scenes lobbying efforts by these powerful interest groups.

Frequently Asked Questions

When would any proposed legislative changes to my benefits actually take effect?

Major structural changes to federal retirement programs rarely take effect immediately. Historically, Congress employs a strategy known as “grandfathering” to protect current beneficiaries and individuals nearing retirement age. If lawmakers raise the retirement age or alter the benefit formula, they typically phase these changes in gradually over a period of ten to fifteen years. This incremental approach attempts to minimize immediate political blowback while allowing younger workers time to adjust their long-term financial planning. However, changes to Medicare premiums or provider networks can take effect much more rapidly, often beginning in the very next enrollment cycle following the legislation’s passage.

Can the president unilaterally alter Medicare or Social Security rules?

The foundational structures of these programs—including tax rates, benefit formulas, and eligibility ages—are established by federal statute and require an act of Congress to change. No president possesses the executive authority to rewrite these core laws unilaterally. However, the executive branch wields substantial administrative power over how these programs operate. The Department of Health and Human Services and the Centers for Medicare and Medicaid Services can adjust coding regulations, alter pilot programs, and tweak the reimbursement models for Medicare Advantage plans. These administrative rule changes do not require congressional approval and can significantly impact the quality and cost of your supplemental coverage.

How does the approaching trust fund depletion shape the current election cycle?

The mathematical deadlines are no longer abstract, distant threats. The latest projections from the Social Security Board of Trustees report indicate that the combined trust funds could face depletion in the middle of the next decade. Upon depletion, the law mandates that the program only pay out the revenue it collects from ongoing payroll taxes—resulting in an automatic, across-the-board benefit cut of roughly twenty percent for all retirees. Because the politicians elected in 2026 will serve crucial terms as this deadline rapidly approaches, they cannot easily evade the issue. The looming cliff forces candidates to go on the record with specific, mathematically viable rescue plans, elevating the topic to a central pillar of the midterm debates.

What specific policy details should I look for when evaluating my local candidates?

You must demand specifics beyond vague promises to “protect seniors” or “save the system.” Evaluate candidates based on the actual mathematical levers they are willing to pull. Ask whether they support lifting the payroll tax cap for earners making over $400,000. Investigate their stance on transitioning to a chained CPI for inflation adjustments. Check their voting records regarding the privatization of healthcare networks or their support for allowing the federal government to negotiate directly with pharmaceutical companies. A credible candidate will acknowledge the impending math problem and explicitly detail whether they prefer revenue increases, benefit adjustments, or a specific combination of both.

Outlook: The Milestones to Monitor

As the 2026 election cycle accelerates, you need to monitor several critical milestones that will clarify the actual policy threats to your benefits. Pay close attention to the September debate stages, where moderators will force candidates to abandon their generalized talking points and address the trust fund insolvency directly. The answers provided under pressure often reveal a candidate’s true legislative priorities and highlight the fractures within their own party coalitions.

Additionally, remain vigilant during the post-election lame-duck legislative session in late 2026. Retiring or defeated lawmakers—freed from the immediate threat of voter retaliation—sometimes partner with leadership to push through unpopular structural reforms or budgetary compromises. By tracking federal election spending, analyzing independent budget projections, and demanding precise answers from your local candidates, you can navigate the political noise and adequately prepare for the fiscal realities of the next Congress.